In 2019, Germany’s non-ferrous foundry sector pulled in over €6.5 billion in revenue. More than 110 plants with 50 or more employees were running at full tilt. It was Europe’s largest die casting market and one of the most important overseas customer bases for Chinese foundries.

Six years later, the number of plants in the same statistical cohort has dropped into double digits, and industry revenue has slipped below €6 billion. COVID, the energy crisis, and the automotive electrification transition hit in succession, driving the sector through a three-phase shakeout: shock, divergence, and restructuring.

This article draws on annual reports from the German Foundry Association (BDG), data from the Federal Statistical Office (Destatis), and industry coverage by GIESSEREI magazine to map the scale, logic, and boundaries of this six-year transformation.

1. Aggregate Picture: Plants Drop Below 100, Revenue Enters Negative Territory

1.1 Plant Count: Slow but Irreversible Attrition

Using Destatis’ uniform classification for non-ferrous foundries (WZ code group “Non-ferrous metal casting,” covering light-metal and heavy-metal die casting and gravity casting, ≥50 employees):

| Year | Non-ferrous foundries (≥50 employees) | YoY change | Industry condition |

|---|---|---|---|

| 2019 | ~112 | — | Cyclical peak, GIFA trade fair year |

| 2020 | ~110 | −2 | COVID shock, staggered automotive supply chain shutdowns |

| 2021 | ~108 | −2 | Nominal order rebound, chip shortages constraining throughput |

| 2022 | ~105 | −3 | Russia–Ukraine war, natural gas price explosion |

| 2023 | ~102 | −3 | Elevated energy costs, SMEs seeking restructuring |

| 2024 | ~96 | −6 | Insolvency law lag effects crystallising; first drop below 100 |

| 2025 | ~94 | −2 | Offshoring trend continuing |

Note: 2024 and 2025 figures are estimates extrapolated from BDG industry trends and existing Destatis series. Destatis full-year statistics typically run 12–18 months behind; final official numbers may adjust slightly. Not every disappearing plant is a liquidation — some count as “reduced” in the statistics because mergers changed the legal entity, even though physical capacity may still exist.

Cumulative loss over six years: roughly 18 plants, a decline of about 16%. The sharp single-year drop in 2024 (−6) represents the delayed release of energy-crisis pressure — small and mid-sized firms that scraped through 2022 on bridge financing finally exhausted their banks’ patience by 2024.

1.2 Industry Revenue: The €6 Billion Floor Gives Way

| Year | Non-ferrous foundry revenue (€B) | Operating backdrop |

|---|---|---|

| 2018 | ~6.8 | Last peak of the internal combustion era |

| 2019 | ~6.5 | Global passenger car output declining |

| 2020 | ~5.1 | Pandemic hammer, Kurzarbeit widespread |

| 2021 | ~5.8 | Chip crisis capping order conversion |

| 2022 | ~6.4 | Nominal revenue inflated by surging aluminium ingot prices and general inflation |

| 2023 | 6.22 | BDG officially confirmed figure |

| 2024 | ~5.7 | EV transition decelerating, die casting orders retreating (estimated) |

| 2025 | ~5.3 | Industry forecast; third consecutive year of real negative growth |

The 2023 figure of €6.22 billion is a traceable BDG public benchmark. The 2024–2025 numbers draw on market estimates from GIESSEREI and industry analysts — they remain subject to adjustment before Destatis releases final annual figures, but the direction is unambiguous: the sector has entered a multi-year contraction.

The long-held industry assumption that “€6 billion is the revenue floor for German non-ferrous die casting” has been undermined by the reality of 2024–2025. The cause is not a single event but the compounding of two negative trends: European domestic BEV demand is falling short of expectations, delaying the release of large gigacasting structural orders; meanwhile, the decline of traditional ICE small-parts volumes is accelerating. The handover between old and new powertrains has produced a vacuum period.

2. Demand Overview: V-Shaped Recovery Followed by Another Stall

Looking at total output (aluminium and magnesium die casting dominant, automotive customers accounting for over 76%):

| Year | Output (thousand tonnes) | Demand condition |

|---|---|---|

| 2019 | ~94.0 | ICE demand peaking and turning down |

| 2020 | ~72.1 | Pandemic collapse, supply-chain meltdown |

| 2021 | ~85.3 | Nominal demand recovery, chip shortage restricting volume |

| 2022 | ~88.5 | Backlog release; energy crisis not yet reflected in output |

| 2023 | 83.5 | BDG official final figure |

| 2024 | ~80.5 | BEV sales below expectations, order softening (estimated) |

| 2025 | ~74.0 | Overall automotive production decline and export weakness (estimated) |

From 2019 to 2025, total output contracted by approximately 21%. The industry had banked on gigacasting and other large electrification-related parts to offset the decline, but the sharp deceleration of European EV adoption in 2024–2025 meant that new demand growth could not fully compensate for shrinking traditional components.

One important caveat: these figures measure tonnage, while average industry pricing is rising. A 60 kg gigacast rear floor pan carries a far higher per-kilogram ex-works price than a basket of 2–3 kg small brackets. A tonnage decline does not translate one-to-one into an equivalent drop in value added — a point explored further in later sections.

3. Efficiency and Profitability: Near-Stagnant Output per Employee, Margins Squeezed from Both Sides

| Year | Output per employee (€K/person·year) | Industry condition |

|---|---|---|

| 2019 | ~19.1 | Normal cyclical conditions, moderate automation |

| 2020 | ~15.7 | Pandemic shutdowns, per-capita output collapse |

| 2021 | ~18.2 | Supply-side constraints, efficiency not fully restored |

| 2022 | ~20.0 | Raw material price surge inflating nominal figure |

| 2023 | 19.0 | BDG benchmark (€6.22B / 32,700 employees) |

| 2024 | ~18.3 | Order decline, under-utilisation (estimated) |

| 2025 | ~18.5 | Marginal stabilisation after workforce reductions (estimated) |

Output per employee = total industry revenue / total industry employment. 2023 is the BDG-confirmed figure; other years are derived from revenue estimates and employment trend data.

Stripping out the nominal distortion from the 2022 raw-material price spike, output per employee in Germany’s non-ferrous die casting sector has essentially flatlined over six years. Meanwhile, labour costs have risen steadily through annual collective bargaining rounds, and energy costs have stabilised at 2–3× their pre-crisis levels. The result is a margin squeeze from both directions — input costs climbing, output value shrinking, and per-capita efficiency offering no buffer.

However, “stagnant output per employee” does not equal “no profitability.” Germany’s top-tier die casters — the European operations of GF and Nemak, for example — still command meaningful pricing power. The technology premium on high-end structural parts partially offsets cost pressures. The real casualties are small and mid-sized plants without pricing power, those dependent on standard-component orders.

4. Polarisation: Multinationals Rebalance Globally, SMEs Suffer Chronic Bleeding

The shakeout has produced a clear bifurcation within German die casting:

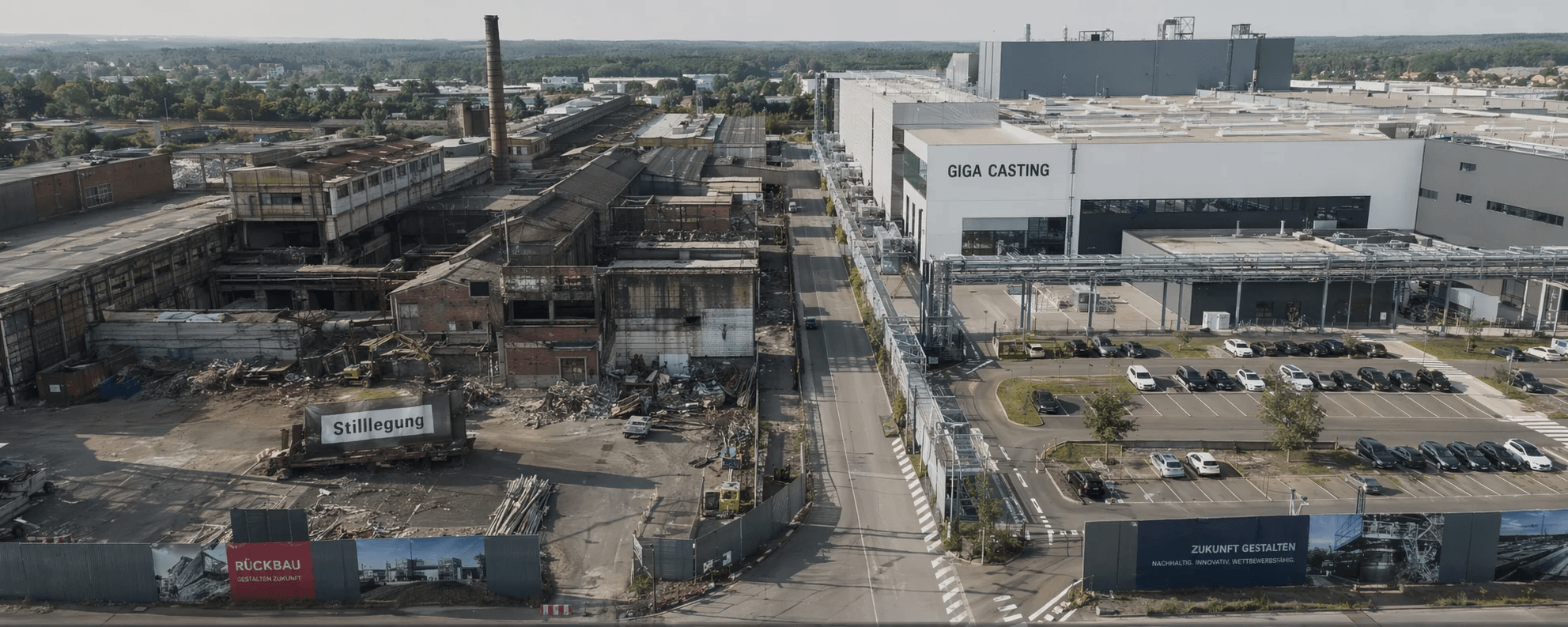

Small and medium-sized family-owned firms (Mittelstand) face an existential squeeze. After the energy crisis, continuing to melt aluminium with gas-fired furnaces directly erodes margins; switching to electric induction furnaces demands capital expenditure in the millions of euros. With demand soft for several years running and banks tightening credit to traditional manufacturing, many SMEs cannot raise that investment. They are being ground down between customer losses and unsustainably high energy costs.

Leading die casting groups have the toolkit to absorb the cost shock. Multinational players such as GF Casting Solutions and Nemak hold two critical advantages: the financial capacity to invest in gigacasting and other high-end production lines, and the ability to reallocate production across borders. When German domestic electricity prices become prohibitive, they can shift portions of order books to plants in Poland, Hungary, or Mexico, using lower local energy and labour costs to offset losses in the home market.

This is not a one-directional narrative of “German decline.” It is a structural restructuring with both winners and losers. Large groups have preserved competitiveness through cross-border footprints and product upgrading; small plants without scale or technological moats are being progressively eliminated. The industry as a whole is “losing plants,” but the survivors are moving up the product-value chain.

5. Gigacasting: Europe’s Capacity Gap

5.1 Capacity Already on the Ground

Europe — including Germany — has been comparatively cautious in committing to gigacasting. The following are publicly confirmed installations of 6,000-tonne and larger die casting capacity:

- GF Casting Solutions (Switzerland/Germany): Deployed Bühler Carat 610 (6,100 tonnes) and Carat 840 (8,400 tonnes) ultra-large systems at its Austrian site and core German production lines, producing integrated front longitudinal members and rear body structures. GF is Europe’s front-runner in gigacasting.

- Nemak (Mexico/Europe): To address the large-format requirements of EV battery trays and e-drive housings, Nemak installed multiple 6,000-tonne-class machines at its European plants, concentrated in Slovakia and lightweight-structure centres near Germany.

- BMW Plant Landshut: BMW invested directly in ultra-large-tonnage die casting machines at its largest German lightweight casting base for large body structural components on the Neue Klasse dedicated EV platform.

- Volvo Torslanda Plant (Sweden): Commissioned a fully automated Bühler Carat 840 (8,400 tonnes) gigacasting line. This is the largest publicly disclosed tonnage installation in the Nordic region.

In addition, firms such as Martinrea Honsel (Meschede, Germany) are undertaking large-tonnage process upgrades.

5.2 The Gap with China

Compared with the Chinese market — where a dozen or more 10,000-tonne-class machines are being rolled out in parallel — Europe’s total installed base of 6,000-tonne-plus gigacasting capacity remains limited. The disparity is not solely a matter of capital willingness. It also reflects load-bearing constraints in ageing European factory buildings, the lead times and permitting requirements for new production lines, and a more cautious technical assessment of the gigacasting route by some European OEMs.

This capacity gap has become more visible in 2025–2026: European EV growth may have slowed, but demand for large integrated structural parts has not gone away — it is simply materialising more slowly than anticipated.

6. Moats That Have Not Disappeared: What Cards Germany Still Holds

If the preceding sections paint a picture of contraction, here is the other side — the structural advantages German die casting still retains:

Materials and process know-how. Germany maintains a lead over China and Eastern Europe in upstream domains such as heat-treatment-free aluminium alloys, high-strength-ductility magnesium alloys, and precision die design. Gigacasting is not merely “buying a machine.” The soft capabilities — runner and gate design, thermal balance control, defect prediction modelling — are accumulated over decades.

Tier-1 relationship barriers. Germany’s leading die casters have decades of co-development history with the engineering departments at BMW, Mercedes-Benz, and Volkswagen. A new entrant seeking to break into these relationships needs more than a price advantage — it must clear lengthy supplier qualification processes, simultaneous-engineering capability validation, and series-production consistency audits.

“Made in Germany” pricing power. In ultra-precision die cast parts — DCT transmission housings, turbocharger centre housings — German plants still deliver the highest global yields and process stability. This preserves a profitable niche: not a large market, but one that cost competition cannot eat away in the near term.

Potential impact of the EU Carbon Border Adjustment Mechanism (CBAM). Should CBAM extend its coverage to aluminium die castings in the coming years, Chinese exports to Europe would carry an additional carbon-cost burden. At that point, the total equation of “low-cost Chinese energy + ocean freight + CBAM” versus “high German electricity prices but zero carbon tariff” becomes more complex — though the outcome depends entirely on the pace of policy development.

This is not “Germany is finished.” It is “the era of easy money is over.” German die casting is being forced to switch lanes — from cost competition to technology-barrier competition. Those that complete the switch will survive, and may even strengthen; those that cannot will be eliminated.

7. Implications for China’s Die Casting Supply Chain

Looking back at this six-year shakeout from a 2026 vantage point, three observations stand out:

First, the cost-differential window is real but time-limited. With German energy costs structurally elevated, Chinese foundries enjoy an objective cost advantage in energy-intensive process steps. For moderately complex die cast parts with higher standardisation and lower technical barriers, Chinese suppliers’ pricing leverage is expanding. The precondition, however, is clearing customer quality audits and supplier qualification — a hurdle that does not get lower just because the cost gap exists.

Second, the gigacasting window is narrowing, not permanently open. Europe’s gigacasting capacity gap creates an opportunity for Chinese foundries to enter European Tier-1 supply chains. But European OEM sourcing lead times typically run 18–24 months, meaning projects initiated today would not reach series production until around 2028. The firms already embedded in customers’ development programmes during the pre-engineering phase will capture the first wave of benefits.

Third, trade-policy risk is accumulating. BDG has repeatedly expressed concerns to Berlin and Brussels about “import pressure from Asian suppliers.” If the EU extends CBAM coverage to aluminium die castings or initiates anti-dumping investigations, Chinese exporters operating on a pure-export model would be the first to feel the impact. Cross-border capacity configurations — “Chinese technology plus local plants in Eastern Europe or Mexico” — may shift from optional to mandatory.

Six years of data trace a clear trajectory: Germany’s non-ferrous die casting industry is undergoing structural contraction — fewer plants, lower tonnage, thinner margins — but this is not an industry collapse. The survivors are moving faster on product upgrading and cross-border footprint expansion. For Chinese die casting enterprises, the key question is not “the Germans are failing” but rather “which products no longer make economic sense to produce in Germany, and which still must be made there.” The direction in which that boundary is moving — that is where the real opportunity lies.

Data sources: BDG Branchenkennzahlen 2023, Destatis industry statistics, GIESSEREI magazine 2019–2026 editions, Statista topic data. 2024–2025 figures are industry estimates pending official final confirmation.