For a solid decade, if you asked a die-casting foundry owner what the European market was buying, the answer came down to three things: engine blocks, transmission housings, and chassis components. The internal combustion powertrain was the industry’s ballast — heavy, reliable, and stable. Or at least it was, until about 2019.

That ballast is now eroding, and not cyclically. The shift from combustion to electric drivetrains isn’t a downturn you wait out — it’s a permanent subtraction from the demand pool for traditional powertrain castings. But at the same time, a set of entirely new demand streams is emerging, driven by the green transition and the build-out of digital infrastructure. And their growth rates, almost across the board, run well ahead of anything the traditional automotive sector has delivered in years.

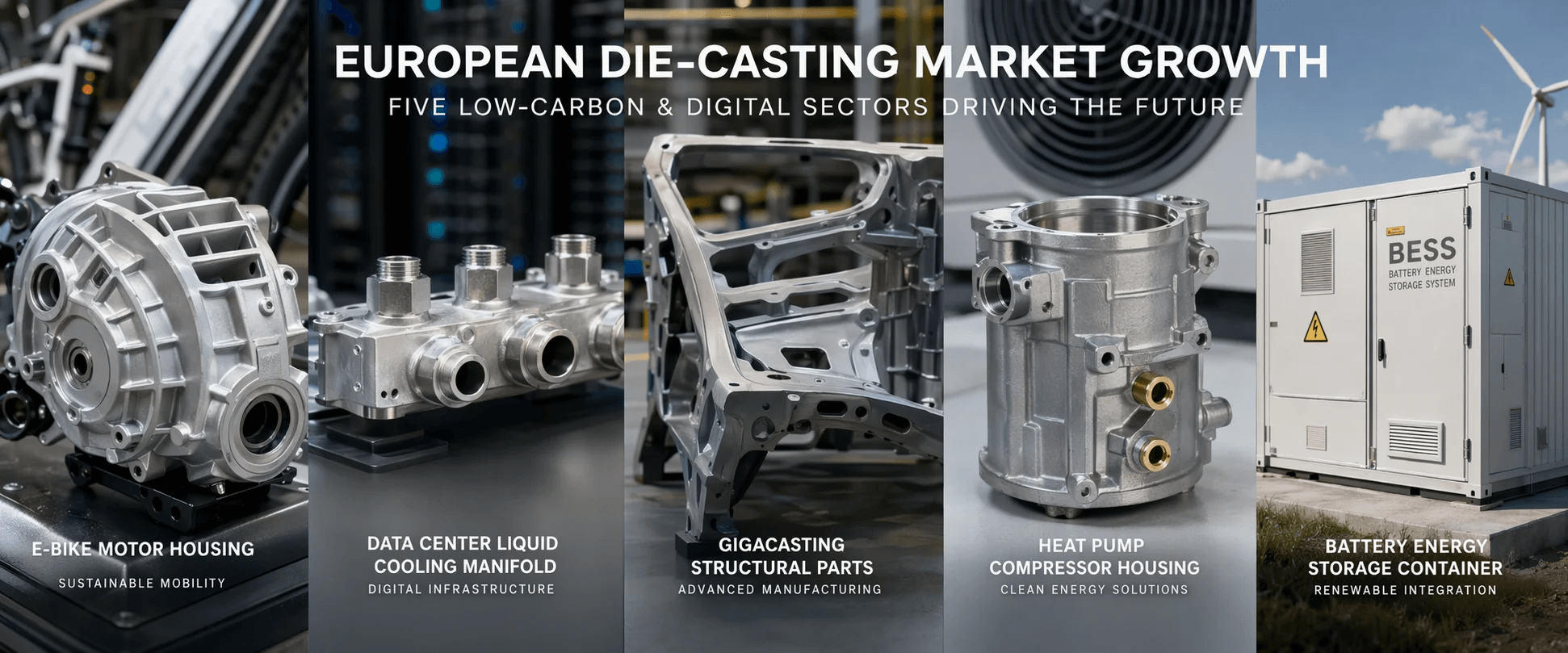

This is Part 1 of a two-part series. Here, we focus on five growth poles tied directly to low-carbon and digital infrastructure: e-bikes, AI data center liquid cooling, EV structural components, heat pumps, and energy storage systems. Each section brings concrete market data and a candid read on what the opportunity actually looks like for a die-casting supplier.

E-Bikes: A Ten-Figure Die-Casting Market Hiding Behind the Automotive Headlines

Europe is the world’s largest market for electric bicycles, and the numbers tell a story of sustained expansion. Estimates vary by research house — some peg the 2025 European e-bike market at roughly $18 billion, growing at a 7.6% CAGR to reach $36.1 billion by 2035. More bullish sources put 2025 closer to $29.4 billion, with a path to $45.1 billion by 2032 at a 12.7% CAGR. The divergence comes down to definitional scope — whether speed pedelecs and cargo bikes are counted in or out, and how many national markets are included. But the directional signal is unanimous: this market is still accelerating.

For the die-casting industry, the interesting number isn’t the total market size. It’s the fact that an e-bike went from using essentially zero die-cast aluminum parts to requiring four to ten kilograms per unit. Traditional bicycles were welded-tube frames, stamped brake parts, extruded rims — die casting had no role. The electric motor changed that entirely.

A mid-to-high-end e-bike now contains a substantial bill of die-cast parts: the mid-drive motor housing and casing (typically the largest and most complex single casting, using ADC12 or AlSi9Cu3 at 1.5 to 3 kg, with integrated heat-dissipation fins); the controller housing; battery mounting and retention structures; steering components; and structural elements for cargo bikes. Taken together, a premium e-bike can carry over eight kilograms of die-cast aluminum.

The growth trajectory is clear, but there is a near-term variable worth watching: the industry is still working through an inventory correction cycle, so quarter-to-quarter growth may not match the explosive post-pandemic surge. From an entry-barrier perspective, though, e-bikes are unusually accessible. Product lifecycles are longer than automotive, certification requirements are simpler, and the customer base is far more fragmented — characteristics that favour mid-sized foundries with precision aluminum die-casting capabilities, without the two-year qualification ordeal that automotive supply chains demand.

AI Data Center Liquid Cooling: A Precision Casting Demand That Didn’t Exist Five Years Ago

If e-bikes represent the electrification of an existing product category, AI data center liquid cooling is something different — a demand pool that has materialised almost from zero.

The explosion in AI training and inference compute is driving a new investment cycle in European data center construction. The European AI data center market was valued at roughly $17.4 billion in 2025, projected to grow from $21.7 billion in 2026 to $65.2 billion by 2031 — a 24.65% CAGR. That kind of growth rate is rare in any industrial segment.

What matters for die casting isn’t the data center itself, but the shift in how those servers are cooled. High-power AI racks, with per-rack power densities routinely exceeding 30 kW, have pushed past the thermal limits of conventional air cooling. Liquid cooling is moving from “nice to have” to “mandatory.” In 2025, liquid cooling accounted for roughly 30.4% of data center cooling investment; by 2031, that share is expected to reach 36.5%. The European data center liquid cooling market alone (excluding the UK) was valued at approximately $1.2 billion in 2024 and is projected to hit $8.9 billion by 2034 — a 22.1% CAGR.

The die-casting opportunity here centers on a specific set of components: CDU (coolant distribution unit) housings, liquid-cooling manifolds, pump bodies and valve bodies, heat exchanger housings, and cold-plate structural components. The requirements are meaningfully different from automotive castings — the priority isn’t lightweighting or crash strength, but corrosion resistance, dimensional stability, and leak-tightness. Cooling fluids circulating for years exert chemical aggression on materials; even minor dimensional deviations can cause leaks, and data centers have exactly zero tolerance for coolant where it shouldn’t be.

The market is in an early, high-growth phase, but there is one risk that demands ongoing attention: the liquid-cooling technology roadmap is still in flux. Cold-plate and immersion-cooling architectures are competing, and the two approaches call for different casting specifications. Which direction a supplier bets on depends on which downstream technology path their customers ultimately commit to.

EV Structural Components: The Weight Is Shifting Inside the Industry’s Biggest Customer

Electric vehicles remain the single most important demand driver for European die casting, and that won’t change anytime soon. But the composition of that demand has already been fundamentally rewritten. Traditional engine blocks and transmission housings are in irreversible decline, while lightweight structural components are taking over as the growth engine.

The European automotive die-casting market as a whole was valued at roughly $16.1 billion in 2025, with a projected path to $22.0 billion by 2031 — a 5.32% CAGR. That headline rate looks modest next to the sectors above, but the absolute volumes are enormous: a single percentage point of growth in automotive releases more die-casting tonnage than the entire addressable market of several emerging sectors combined. Within this total, lightweighting-driven aluminum die-cast components are expected to reach €8.2 billion, and gigacasting alone accounts for over 40% of the incremental growth — making it the single most important engine inside the engine. The European automotive aluminum die-casting components market, narrower in scope, was valued at roughly $5.6 billion in 2024 and is projected to reach $9.5 billion by 2033, a 6.10% CAGR.

The gigacasting logic is straightforward: replace up to 100 small stamped-and-welded parts with a single aluminum structural casting weighing over 100 kilograms. Volkswagen, Volvo, and other mainstream European OEMs have publicly committed to this technology roadmap — it is no longer a Tesla-only experiment.

But for die-casting suppliers, this is also the highest-barrier opportunity in the landscape. Gigacasting demands investment in ultra-large presses (6,000 tonnes and above) and deep process capability — particularly in the development and application of heat-treatment-free aluminum alloys. It is a play for well-capitalised Tier-1 foundries. For mid-sized operations, the more realistic path may be secondary supply into the gigacasting ecosystem: machining, surface treatment, or sub-assembly work on gigacast components.

Heat Pumps: Policy-Driven Demand With Long-Term Visibility

Driven by the twin engines of European energy transition policy and building-efficiency regulation, the heat pump market offers one of the most predictable growth curves of any sector covered here — because its demand isn’t driven by discretionary consumer preference, but by legislation and subsidy.

The European heat pump market was estimated at roughly $14.2 billion in 2024, expected to reach $16.8 billion in 2025 and $82.6 billion by 2034, at a 19.3% CAGR. Air-source heat pumps — the dominant subcategory — were valued at approximately $9.5 billion in 2025 and are projected to hit $62.8 billion by 2035.

In unit terms, the European Heat Pump Association (EHPA) reports that sales across monitored countries surpassed 2.6 million units in 2025, with steady year-on-year growth. The EU has set a strategic target of 60 million installed heat pumps by 2030 — a number that, if achieved, implies average annual additions of over 10 million units between now and the end of the decade.

The die-cast part categories in a heat pump are relatively concentrated: compressor housings, pump bodies and valve bodies, and heat exchanger structural components. The common thread is high-volume, slow product-cycle parts — once a casting is qualified into a heat pump platform, the supply relationship tends to be sticky. For a foundry, this is the closest thing to a “base-load” customer that exists outside of automotive.

One major caveat: heat pump demand is highly sensitive to national subsidy regimes. Germany, France, and other major markets have repeatedly adjusted heat pump incentives in recent years due to fiscal budget pressures, and these policy swings can create sharp short-term demand volatility. Betting the factory on heat pumps alone would be reckless. But as one pillar of a diversified portfolio, they offer a level of long-term demand certainty that is hard to find elsewhere.

Energy Storage: The Fastest-Growing, Highest-Volume, Least-Settled Sector

Among all the low-carbon die-casting demand streams in Europe, energy storage systems (ESS) are growing the fastest — and are also the least structurally settled.

The European battery energy storage system (BESS) market was estimated at roughly $21.3 billion in 2025, on a trajectory to $54.7 billion by 2030 — a 20.72% CAGR. In capacity terms, EU member states added 27.1 GWh of new battery storage installations in 2025, a 45% year-on-year increase, bringing cumulative operational capacity to 77.3 GWh. By the end of 2025, total installed storage capacity across the wider European region had broken through the 100 GW mark, reaching 102.7 GW. Utility-scale battery storage was the primary growth engine, contributing roughly 55% of additions, while commercial and industrial (C&I) storage deployments grew by 31%.

The die-casting footprint in ESS is broad: PCS (power conversion system) enclosures, BMS (battery management system) controller housings, battery pack structural components and cooling system parts, and high-voltage electrical connectors. Among these, battery pack structural components represent the largest single-order volumes — a single utility-scale storage project can involve hundreds of battery packs, each requiring its own set of cast structural elements.

The current ESS market is still dominated by utility-scale projects, meaning demand for castings tends toward large batch sizes with high customer concentration. The C&I and residential storage segments are smaller today but growing rapidly, with a far more fragmented customer base — for mid-sized foundries, these two sub-segments may offer a more practical and sustainable entry point than chasing utility-scale direct supply.

The five sectors covered in Part 1 share a common underlying logic: they are all offspring of decarbonisation and digitisation. E-bikes represent mobility decarbonisation, heat pumps building decarbonisation, energy storage grid decarbonisation, EV structural components the continuation of transport decarbonisation, and AI data center liquid cooling the direct material demand of digital infrastructure build-out. Their compound annual growth rates range from roughly 5% to 25% — well above the growth rate of European manufacturing as a whole.

In Part 2, we turn to five additional sectors — growth areas tied more directly to traditional manufacturing upgrades and supply-chain restructuring. Their growth logic differs from the low-carbon and digital tracks covered here, but they are no less worth taking seriously.