In January 2020, the halls of the Nuremberg exhibition centre were packed. EUROGUSS — Europe’s flagship die-casting trade fair — had drawn 754 exhibitors from 36 countries. Roughly 15,000 trade visitors squeezed through the aisles. It was, to borrow a phrase the industry would later cling to, the last “normal” winter. Two months later, COVID-19 swept across the globe. Automotive supply chains froze within weeks. And in the six years since, European die casting has never found its way back to that starting line.

What followed was not a single crisis with a single recovery curve. It was — and still is — a cascade of disruptions that landed differently in every country. A pandemic that throttled demand. An energy shock that hit German foundries harder than Turkish ones. An electric-vehicle transition that concentrated gigacasting investment in the hands of a few. And, from January 2026, a carbon border adjustment mechanism that rewrites the arithmetic of importing aluminium castings into the EU.

This is the story of an industry that stopped moving as one.

1. A Europe Out of Sync

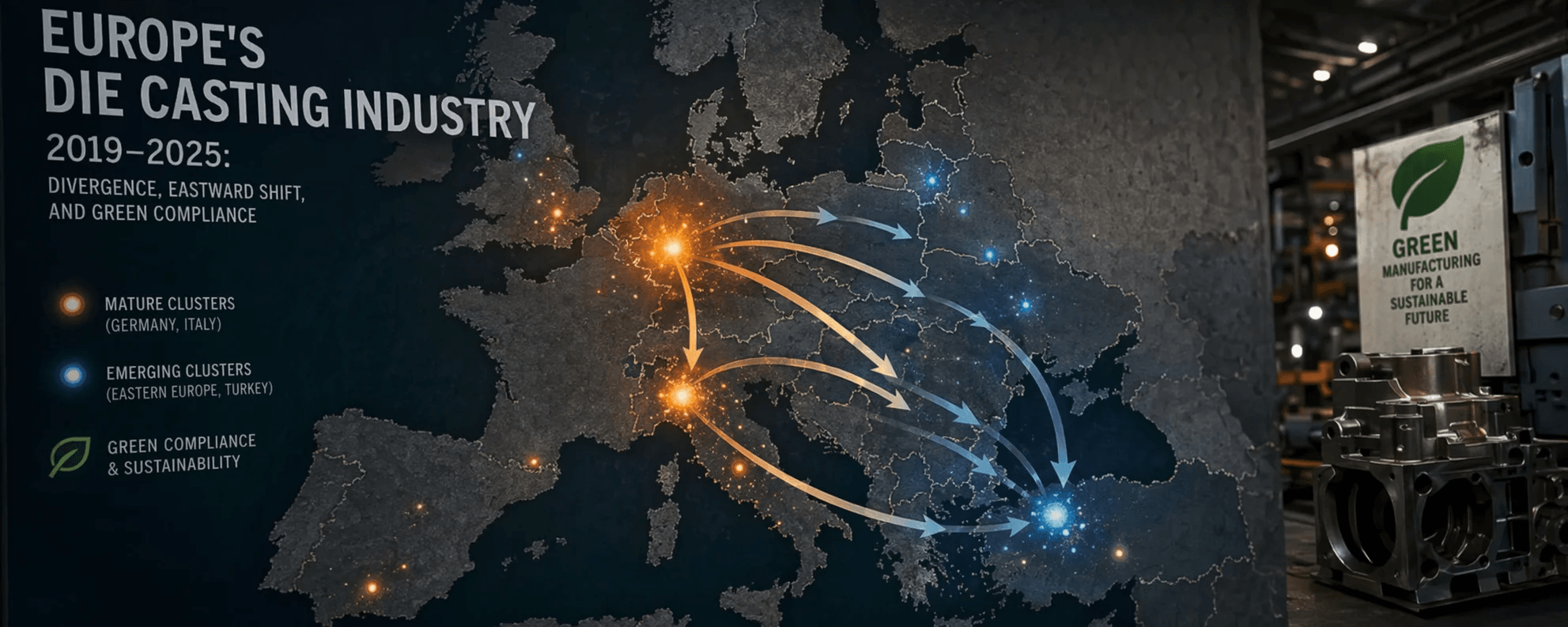

Europe is the world’s second-largest casting production region after China, turning out over 13 million tonnes of castings annually, roughly 30% of which are non-ferrous. But the word “Europe” increasingly masks more than it reveals. Over the past six years, the trajectories of the major producing countries have diverged so sharply that treating them as a single market is no longer useful.

Core Country Output Trends

The table below compares 2019 and 2024 casting output for Europe’s major producers, based on WFO global casting census data and national association figures:

| Country | 2019 total casting output (million tonnes) | 2024 total casting output (million tonnes) | Six-year trajectory |

|---|---|---|---|

| Germany | ~5.0 | ~4.0 | Persistent contraction; hardest hit by energy costs |

| Italy | ~2.3 | ~2.0 | Volatile decline; Q2 2025 down 5.9% year-on-year |

| Turkey | ~2.1 | ~2.5 | Counter-cyclical growth; now Europe’s No.2 |

| France | ~1.5 | ~1.3 | Moderate decline; ahead on green transition |

| Spain | ~1.2 | ~1.1 | Mild shrinkage |

| Poland | ~0.8 | ~0.9 | Absorbing relocated German capacity; slight growth |

| Others (Czechia, Austria, Sweden, etc.) | ~2.1 | ~2.0 | Broadly stable with pockets of growth |

Note: Total casting output includes both ferrous and non-ferrous castings. National statistical coverage (e.g. whether micro-enterprises with fewer than 50 employees are included) varies by country. The figures above represent the orders of magnitude commonly cited across the industry. 2024 data draws partly on WFO census estimates and association forecasts; final official figures may see minor revisions.

The story these numbers tell is one of a widening east-west gradient. Germany and Italy remain the two largest markets by volume, but under the combined weight of energy costs, labour constraints, and environmental compliance, the incremental capacity growth is increasingly happening in what you might call the “cost corridor” — Turkey, Poland, Czechia, and neighbouring countries.

The Non-Ferrous Divergence Runs Deeper

If you isolate non-ferrous casting — predominantly aluminium and magnesium die casting — the divergence is even starker. Take Germany, Europe’s largest non-ferrous die-casting market: the number of non-ferrous foundries and die-casters with 50 or more employees fell from roughly 112 in 2019 to approximately 94 by 2025. Revenue contracted from around €6.5 billion to roughly €5.3 billion. Output shrank by an estimated 21% cumulatively. Over the same period, Turkey’s aluminium die-casting capacity expanded steadily — its foundry sector as a whole climbed from Europe’s third-largest to its second, and sits at seventh globally.

Europe’s total non-ferrous casting output is estimated at 3.0–3.5 million tonnes per year. Germany accounts for roughly 25%, Italy about 18%, Turkey roughly 15%, with France and Spain each at 8–10% and the remainder spread across Eastern and Northern Europe. Over the past six years, Germany’s share contracted while Turkey’s and Poland’s expanded. European die casting hasn’t shrunk in absolute terms — but the distribution of weight inside it has shifted.

EUROGUSS as a Barometer

EUROGUSS, held every two years in Nuremberg, serves as the industry’s de facto health check. Its exhibitor and visitor numbers are a reasonably good mirror of sector sentiment:

| Year | Exhibitors | Countries | Trade visitors | Notes |

|---|---|---|---|---|

| 2018 | 641 | 33 | 15,354 | Benchmark year at cyclical peak |

| 2020 | 754 | 36 | ~15,000 | All-time high; four halls fully booked |

| 2022 | 641 | 36 | 10,707 | Postponed to June due to COVID; visitors down 29% |

| 2024 | 643 | 33 | 14,341 | Exhibitor count back to 2018 levels |

| 2026 | 710 | 38 | 13,986 | Official LinkedIn figures |

Sources: NürnbergMesse closing press releases for each EUROGUSS edition, plus official LinkedIn; 2026 exhibitor, country, and visitor data from EUROGUSS official LinkedIn.

Exhibitor numbers peaked at 754 in 2020 before the 2022 edition pulled back to 641 — but that pullback had less to do with industry contraction than with the fair being forcibly moved from January to June, which made it impossible for many international (especially Asian) exhibitors to attend. The 2024 edition recovered to 643 exhibitors and 14,341 visitors — exhibitor numbers back to 2018 levels, though visitor numbers still lagged pre-COVID figures. By 2026, exhibitors jumped to 710 (+10.4% vs 2024), with participating countries expanding from 33 to 38 — a new high for the fair’s international reach.

A structural shift worth noting: Earlier EUROGUSS editions were dominated by exhibitors from Germany, Italy, Switzerland, and the traditional die-casting heartlands. By the 2026 edition, industry observers pointed out that Chinese die-casting equipment manufacturers “are no longer positioning themselves merely as low-cost alternatives but are increasingly competing on technical capability” — companies like Yizumi, Haitian, and LK Group moving from the margins toward centre stage, redrawing the competitive map of the European die-casting supply chain.

2. Energy: Different Countries, Different Wounds

The energy crisis hit every European foundry. But the depth of the wound varied enormously depending on a country’s pre-war energy mix.

Germany took the deepest hit. Before 2022, roughly 60–70% of the energy consumed by German foundries came from Russian pipeline gas. When the war broke out, Dutch TTF natural gas futures surged from €20–30/MWh to €200–300/MWh, touching €340 at the peak. Even after the German government introduced electricity and gas price brakes (Strompreisbremse and Gaspreisbremse), energy costs once the subsidies expired stabilised at two to three times pre-crisis levels. At the 2023 GIFA trade fair, BDG president Clemens Kuepper publicly called for an “industrial electricity price” to preserve competitiveness. Dr. Heike Denecke-Arnold, COO of thyssenkrupp, put it more bluntly: “A situation the entire post-war era has never faced.”

Italy was wounded, but showed more resilience. Italy was less dependent on Russian pipeline gas than Germany, relying more on North African supplies and LNG — but electricity prices still rose sharply. By August 2025, Italian foundry output was down 5.9% year-on-year. Assofond president Zanardi, commenting on US-EU trade relations, noted that “an agreement with Trump could reduce uncertainty, but Europe must act now to stimulate production.”

France and Spain had relatively favourable energy structures. France’s high nuclear share and Spain’s substantial renewable penetration meant foundries in both countries faced smaller energy cost increases than their German and Italian counterparts. This goes a long way toward explaining why France has consistently outperformed Germany in the FISI (European Foundry Industry Sentiment Indicator).

Turkey became an energy haven. Turkey’s energy costs also rose, but the relative increase was far smaller than in core EU countries. Combined with the lira’s depreciation, which delivered export price advantages, Turkey’s foundry sector sustained growth throughout the crisis. This is one of the core reasons Turkey overtook Italy around 2024 to become Europe’s second-largest casting producer.

3. Gigacasting: A Highly Concentrated Game

Unlike the Chinese market, where dozens of 10,000-tonne-class die-casting machines have been deployed in parallel, Europe’s investment in large-scale structural gigacasting is concentrated in the hands of a very small number of players.

Publicly confirmed 6,000-tonne-and-above die-casting capacity includes:

- GF Casturing Solutions (Switzerland/Germany): Deployed Bühler Carat 610 (6,100 tonnes) and Carat 840 (8,400 tonnes) systems

- Handtmann (Germany): Became Europe’s first Tier-1 supplier to implement megacasting in May 2024

- BMW Landshut plant (Germany): Produced 3.1 million castings in 2025, including large structural body components

- VW Kassel plant (Germany): Confirmed large casting series production in March 2024

- Volvo Torslanda plant (Sweden): Bühler Carat 840 fully automated production line

- FOMA (Italy): Installed a 4,600-tonne Italpresse die-casting cell in November 2025

The concentration is the point. Six companies — four in Germany, one in Sweden, one in Italy. No other major European die-casting country has gigacasting investment at scale. Chinese die-casting equipment manufacturers (Yizumi, Haitian, LK) have begun appearing at EUROGUSS — and the 2026 edition’s industry commentary noted that Chinese manufacturers are “no longer positioning themselves merely as low-cost alternatives but are increasingly competing on technical capability.” Haitian has even set up a local assembly line in Brescia, Italy.

For European OEMs, this concentration creates a capacity bottleneck. For non-European suppliers who can clear the 18-to-24-month qualification timeline, it creates a window — but a narrow one.

4. CBAM and Green Compliance: A New Barrier to Entry

On 1 January 2026, the EU Carbon Border Adjustment Mechanism (CBAM) entered full effect. For the die-casting industry, this means imported aluminium castings from non-EU countries will carry an additional carbon cost calibrated to the EU Emissions Trading System price.

CBAM’s impact on the competitive landscape cuts both ways:

- For EU-based foundries, it provides a layer of “carbon protection” — high-carbon imported aluminium castings lose their price advantage.

- For non-EU exporters, it adds compliance costs and a carbon data reporting burden. Chinese manufacturers who continue to use coal-fired electricity for aluminium production destined for European export will face a meaningful price disadvantage.

Concurrently, the EU Industrial Emissions Directive (BREF) set binding Best Available Techniques (BAT) requirements for the foundry sector in December 2024. This means that regardless of which European country a plant operates in, the minimum bar for environmental compliance is rising everywhere. For smaller foundries, the challenge is no longer just market competition — it is a regulatory survival threshold.

5. What This Means for the Global Supply Chain

Europe’s six-year fragmentation of its die-casting industry sends several signals to global suppliers:

The market hasn’t disappeared — it’s moved. Europe’s total casting demand remains enormous. Over 13 million tonnes of annual casting output, with 3.0–3.5 million tonnes of non-ferrous castings, is a base load that isn’t going away. But the centre of gravity inside that base is shifting from Germany and Italy toward Turkey, Poland, and Czechia. A supplier strategy built solely around German customers will miss the incremental growth markets.

Gigacasting is a ticket to the game, not a dividend. Europe’s gigacasting capacity gap creates an entry opportunity for qualified non-European die-casters — but the window is time-limited and the barrier to entry is high. European OEM supplier qualification cycles typically run 18 to 24 months. Only those who can complete certification within that window will be in a position to compete.

CBAM has rewritten the cost formula. The old arithmetic — “low Chinese electricity prices + ocean freight = landed cost advantage” — now has a carbon-cost term added to it. This means Chinese die-casting exporters’ European strategy needs to evolve from pure export toward a combination of localised production and compliant carbon data. Cross-border capacity configurations — Chinese technology paired with local plants in Turkey or Eastern Europe — may shift from optional to essential.

Europe’s internal divergence is itself an opportunity. The more expensive Germany becomes, the more attractive Turkey and Poland look — and both markets currently have far less mature local supply chains than Germany. For suppliers with the capability to set up in Turkey or Eastern Europe, or to form partnerships with local foundries there, this represents a new route into the European market — one that didn’t exist in a meaningful way a decade ago.

In six years, European die casting went from “one market” to “several.” Germany is bleeding capacity. Turkey is filling the gap. Italy is wrestling with margin compression. Eastern Europe is absorbing what moves east. For global suppliers, the question is no longer “is Europe still viable?” — it’s “which Europe is worth betting on.”

Sources: BDG Branchenkennzahlen 2023; WFO Global Casting Census; CAEF / European Foundry Federation; EUROGUSS 2020, 2024, and 2026 trade fair data; GIESSEREI magazine; Foundry Planet industry reports; FISI European Foundry Industry Sentiment Indicator. Some figures are industry-level estimates; final values may be subject to revision upon publication of national statistical office data.