In Part 1, we unpacked five die-casting growth poles directly tied to low-carbon transition and digital infrastructure — from e-bike motor housings to AI data center liquid-cooling manifolds. Those sectors share a common engine: demand driven simultaneously by policy and technology, with growth rates that run an order of magnitude above anything the traditional automotive segment has produced in years.

But if you only look at the low-carbon and digital tracks, you are seeing exactly half the picture. The other half sits behind far higher walls — in medical devices, industrial robotics, aerospace and defense, and unmanned aerial systems. The logic across these five domains is not “run fast” but “stand firm.” Their certification cycles routinely span two to three years. Product lifecycles stretch five to ten years. And once a supplier is locked into the chain, switching costs make dislodging them extraordinarily expensive. In other words, these are textbook moat markets: high barriers, high margins, high stickiness.

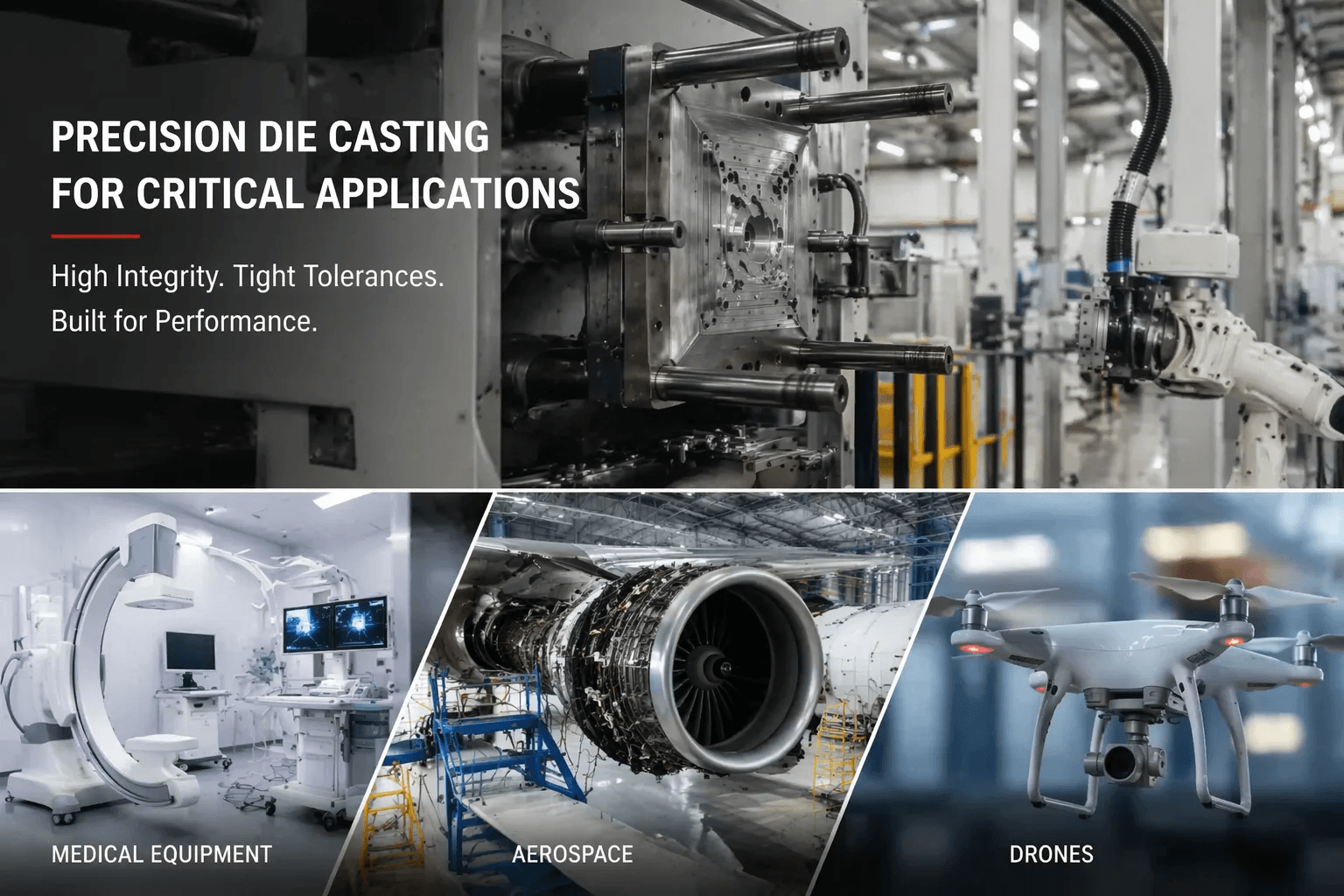

What follows is a sector-by-sector breakdown of the die-casting opportunity, process landscape, and entry barriers across five hardcore manufacturing domains, anchored in the latest available data.

Medical Devices: A Stable Gold Mine the Die-Casting Industry Keeps Underestimating

The European medical device market is enormous and grows with near-boring predictability. The market was valued at roughly $142.17 billion in 2024, expected to reach $148.3 billion in 2025 and $207.39 billion by 2032 — a 4.9% CAGR. A separate research house sees Europe’s medical device market hitting $305.01 billion by 2033. Either way, the vector is clear: slow, steady, relentless expansion.

Behind that vast end-market sit CT scanners, MRI machines, ultrasound systems, anaesthesia workstations, ventilators, and surgical robots — all of which consume high-precision aluminum die castings as core structural components. The global medical component manufacturing market was valued at approximately $16.12 billion in 2024 and is projected to reach $25.23 billion by 2033, a 5.1% CAGR.

The business logic here operates on an entirely different cadence from automotive. Product lifecycles are measured in five to ten years, not five to seven model years. Order volumes sit in the thousands-of-units range — modest by automotive standards — but per-unit value is far higher than commodity industrial components, because the customer is not buying a price; they are buying absolute reliability. A die-cast housing inside a CT scanner cannot have porosity. It cannot exhibit dimensional drift. And it absolutely cannot fail in the field — a medical device field failure is not a warranty claim; it is a patient-safety incident.

Unlike the violent swings of the automotive cycle, medical device demand barely notices economic downturns. Recessions do not stop people from getting sick, and hospitals do not stop refreshing aging equipment because GDP dipped. But the entry threshold is punishingly high. A company must establish and rigorously operate a quality management system compliant with ISO 13485 and other medical industry standards. The documentation rigour and traceability demands under this framework go well beyond what IATF 16949 requires. This is not a market you “dip your toes into.” For the foundry willing to absorb the certification investment, however, it represents one of the most cycle-resistant revenue streams in precision manufacturing.

Industrial Robots and Automation: A High-Growth, High-Divergence Precision Casting Track

European manufacturing’s automation upgrade rolls onward. As the world’s second-largest industrial robot market, Europe is projected to expand at a 15.7% CAGR between 2025 and 2032 — a growth rate that turns heads in any industrial sub-segment.

That said, there is a near-term disturbance worth acknowledging. Weighed down by slowing investment in Europe’s traditional automotive sector, the European collaborative robot market was among the slowest-growing regions globally in 2024–2025. The implication is that demand for robot-related die castings is undergoing clear structural divergence: components for traditional automotive welding robots are decelerating, while demand in surgical robotics and warehouse logistics automation continues to grow at a healthy clip.

From the die-casting standpoint, the industrial robot body relies heavily on high-precision aluminum castings. Joint housings — the articulation points connecting a robot’s six axes — demand levels of roundness and wall-thickness uniformity that make most automotive castings look forgiving by comparison. Reducer housings — the enclosures for harmonic and RV reducers — require exceptional dimensional stability, because micron-level deformation translates directly into lost transmission accuracy. Servo motor housings and robot arm structural components bring a further constraint: lightweighting here is not nice-to-have, it is a hard requirement. Every kilogram shaved off an arm adds a kilogram of effective payload capacity at the end effector.

In aggregate, industrial robots represent a meaningful application direction for precision die casting. But the near-term pressures the European market is absorbing mean that growth momentum is structurally bifurcated, and understanding that bifurcation matters more than staring at the headline growth rate. If the objective is to enter this market, the smarter play is to prioritize customers in surgical robotics and warehouse logistics automation — their order stability is dramatically better than anything coming out of traditional automotive welding lines.

Aerospace: The Longest Certification Cycle, the Deepest Moat

As global civil aviation traffic continues its post-pandemic recovery and European aerospace manufacturing expands capacity, demand for lightweight components keeps rising. Europe remains one of the world’s most important aerospace manufacturing hubs. Take Airbus: as of end-2025, cumulative orders for the A320 family stood at roughly 20,000 aircraft, with over 7,000 still in backlog awaiting delivery. Airbus plans to ramp A320 family monthly production to 70–75 units by 2027 — a rate increase that will pull continuously on the European aerospace supply chain.

One point needs to be made clearly, because it is easily misunderstood: aerospace manufacturing employs an exceptionally diverse process palette. Investment casting, sand casting, gravity casting, forging, and machining still account for the overwhelming share. High-pressure die casting in aerospace is concentrated in select non-critical structural applications — aircraft cabin system components, seating and interior structural parts; actuator housings and avionics enclosures; and satellite and spacecraft auxiliary structures plus UAV structural components. In plain terms: nobody is putting an HPDC part in a turbine blade or landing gear assembly. But inside the cabin, in the electronics bay, and across unmanned airframes, die castings are everywhere.

The aerospace sector combines sky-high certification barriers with extraordinary customer stability. Entry typically demands establishment of an EN 9100 (AS9100) aerospace quality management system, and the certification timeline is measured in years, not months. The sector’s headline growth rate does not match what you see in digital energy and other emerging industries — aerospace is more a heavy freight train running at constant speed than a rocket — but per-part value added is exceptional and supplier switching costs are immense. This is a moat market tailor-made for long-term positioning by companies with top-tier precision manufacturing capability.

Defense Equipment: Surge in Military Spending Creates Deterministic Demand

Of the five sectors covered here, this is the one with the most direct and most unusual growth driver.

The geopolitical shifts of recent years have triggered sustained defence budget increases across Europe. Data from the Stockholm International Peace Research Institute (SIPRI) shows total European military expenditure surged to $864 billion in 2025, a 14% year-on-year jump, marking an all-time high. Germany has now posted double-digit defence spending growth for three consecutive years. EU-27 defence expenditure reached €381 billion in 2025, a sharp spike from prior levels.

These are not just news headlines — they are translating into real industrial orders. The relevant die-casting applications fall into three buckets: auxiliary components for armoured vehicles — non-load-bearing brackets, covers, pipe fittings and connectors; structural components for military UAVs — airframe frames, wing ribs, hardpoints and pylons, where the lightweighting and specific-strength requirements run higher than anything in the civilian domain; and housings for radar systems, communication equipment, and electro-optical payloads — these electronics enclosures typically need to deliver both electromagnetic shielding and thermal dissipation, imposing additional constraints on material formulation and process windows.

Defence orders are exceptionally stable and margins are generous. A number of European die-casting companies that historically served the automotive sector — GF, Nemak among them — have begun expanding into defence. But one reality must be acknowledged with clear-eyed honesty: tight export controls, security clearance requirements, and local supply-chain protection policies make it exceedingly difficult for Chinese die-casting companies to enter as Tier-1 or Tier-2 suppliers directly. The more realistic path is to have a local production base in Europe, or to participate indirectly through a European joint-venture partner. This is not a market a price-competitiveness advantage can pry open.

Drones: Still Small in Scale, but the Growth Rate Commands Attention

Europe’s commercial and industrial UAV market continues to expand. The 2025 market was estimated at approximately $7.58 billion, expected to reach $8.52 billion in 2026 and $15.23 billion by 2031 — a 12.34% CAGR. Europe now counts over 1.6 million registered drone operators, and application scenarios in industrial surveying, logistics delivery, and agricultural spraying are opening up rapidly.

Typical die-cast components cluster in a few categories: motor mounts and battery frames — the foundational structure of every airframe, with strength-to-weight demands that border on unforgiving; gimbal structural components, camera housings, and landing gear — parts that need to be not just light but also capable of maintaining precise positioning under sustained vibration.

For now, the drone market as a whole remains modest next to new energy vehicles — it is nowhere near a segment that can substitute for automotive revenue volumes. But it is growing fast, and the material performance demands — particularly for high-specific-strength aluminum-magnesium alloy die castings — happen to be capabilities many foundries have already built in the course of automotive lightweighting work. As Europe’s drone regulatory framework matures, particularly around EASA airworthiness and operational rules, this segment has the potential to become a highly active innovation growth point for precision die castings. The play now is not about near-term revenue; it is about securing a position three to five years down the road.

Part 1 examined five “run fast” low-carbon and digital tracks. The five domains in Part 2 tell a different story — slow, difficult, but stable. ISO 13485 for medical devices. AS9100 for aerospace. Security clearance for defence. Each one is a high wall. But on the other side of those walls sit five-to-ten-year stable order books and margins that leave commodity industrial products in the rear-view mirror.

Europe’s manufacturing centre of gravity is shifting from “scale first” to “value first.” Die-casting demand from traditional ICE powertrains is entering a structural decline — this is not a cyclical correction, it is a permanent volume reduction driven by powertrain architecture switching. But at the same time, the low-carbon digital tracks and the high-end equipment tracks are simultaneously opening two distinct demand gaps. The former rewards speed. The latter rewards barriers.

For die-casting companies with the capability to clear certification thresholds, the better move is not to keep grinding on scale and price wars inside the single automotive vertical, but to allocate a portion of precision capacity toward these high-end equipment domains. Building a customer portfolio that spans automotive, medical, aerospace, defence, and industrial automation is, at its core, a structural hedge against single-industry cyclical risk. It is not just a market expansion — it is a fundamental upgrade of the company’s resilience architecture.